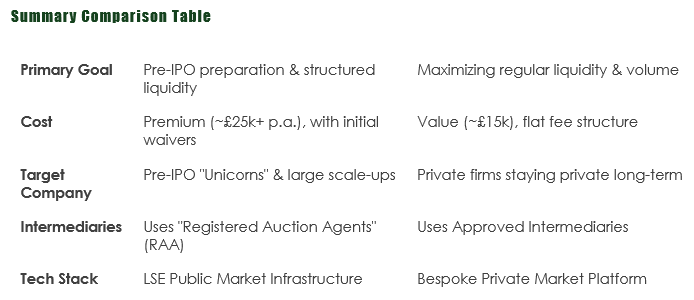

The primary distinction lies in their trading mechanisms and strategic positioning. The LSE positions its venue as a premium "stepping stone" to public markets, while JP Jenkins focuses on maximizing liquidity through more frequent trading windows.

1. Trading Model & Frequency

LSE Private Securities Market (PSM):

JP Jenkins PISCES Venue:

2. Cost Structure

LSE PSM:

JP Jenkins:

3. Strategic Positioning & Target Audience

LSE PSM:

JP Jenkins PISCES Venue:

Regulatory Context for Both Platforms

Regardless of the platform, both operate under the Government’s 2025 PISCES regulations and the FCA’s sandbox PISCES sourcebook, which means:

This website uses cookies or similar technologies, to enhance your browsing experience and provide personalized recommendations. By continuing to use our website, you agree to our Privacy Policy